Over the past two decades, investment in Kazakhstan’s mining industry has gone through several distinct phases — a period of steady growth, an investment peak, and a subsequent correction. Thus, while in 2005 capital investment in mining and quarrying amounted to 707.2 billion tenge, by the peak year of 2019 it had increased nearly eightfold, reaching a record 5.6 trillion tenge. Growth was accompanied by several investment surges, the most notable occurring in 2009 (plus 48%), 2018 (plus 51.1%), and 2019 (plus 24.5%). These periods were associated, among other factors, with the implementation of major oil and gas projects and the active expansion of extraction infrastructure.

After the 2019 peak, the investment trajectory changed. As early as 2020, capital investment declined by 26%, to 4.1 trillion tenge, and the downturn continued in 2021. This was partly influenced by the pandemic-related crisis, but not exclusively: although the sector saw a partial recovery in 2022 and 2023, it subsequently re-entered a contraction phase. By the end of 2024, capital investment in the mining industry decreased in value terms by 23.1%, to 3.7 trillion tenge (physical volume index — 79.9%), and in 2025 it fell by a further 12.3%, to 3.2 trillion tenge (physical volume index — 85%). As a result, over two years, investment in the sector declined by more than one-third compared to 2023 levels. The trend is also confirmed by data for the beginning of the current year: in January 2026, capital investment in mining and quarrying amounted to 196.5 billion tenge, down 10.3% year-on-year (physical volume index — 83.5%).

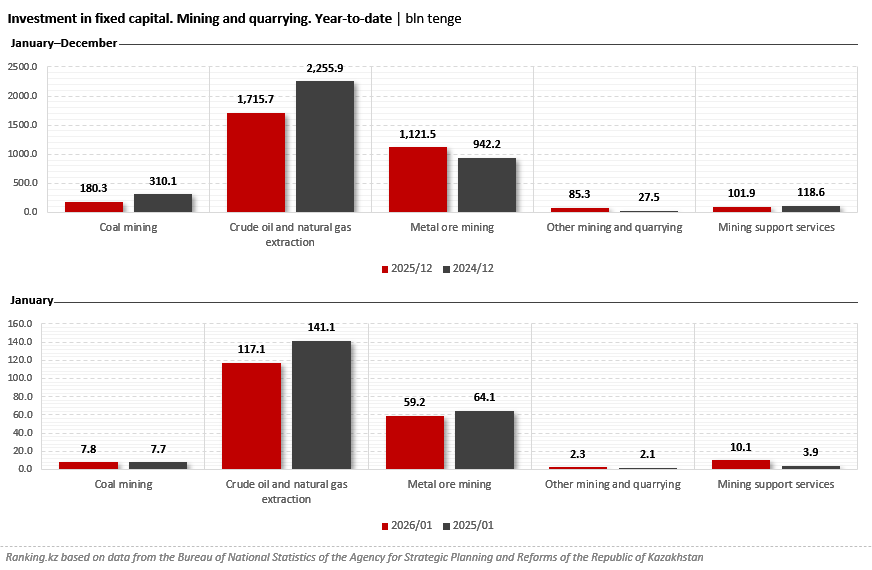

By type of activity, the oil and gas sector made the largest contribution to the decline in investment volumes in 2025. Investment in crude oil and natural gas extraction fell by 23.9%, to 1.7 trillion tenge. A significant decrease was also recorded in coal mining: minus 41.8%, to 180.3 billion tenge. Against this backdrop, notable growth was observed only in metal ore mining, where investment increased by 19%, to 1.1 trillion tenge. In the segment of other mining and quarrying, investment more than tripled, reaching 85.3 billion tenge, although the absolute volume remained relatively modest. Investment in mining support services declined by 14.1% year-on-year, to 101.9 billion tenge.

In January 2026, the picture was somewhat different: the oil segment continued to contract (down 17%, to 117.1 billion tenge), investment in metal ore mining also declined (down 7.7%, to 59.2 billion tenge), while investment in mining support services showed a sharp increase (2.6-fold, to 10.1 billion tenge). Capital investment in coal mining remained virtually unchanged (up 0.2%, to 7.8 billion tenge), while investment in other minerals increased (up 11.5%, to 2.3 billion tenge).

An additional source of uncertainty for investment activity remains the situation in the global oil market. In recent days, oil prices have shown heightened volatility, reacting to geopolitical risks, fluctuations in expectations for global demand, and signals from major producers. For oil extraction projects that require significant capital investment and long investment cycles, such price volatility increases risk levels. As a result, companies often postpone or revise investment plans, which may further constrain investment dynamics in the extractive sector.