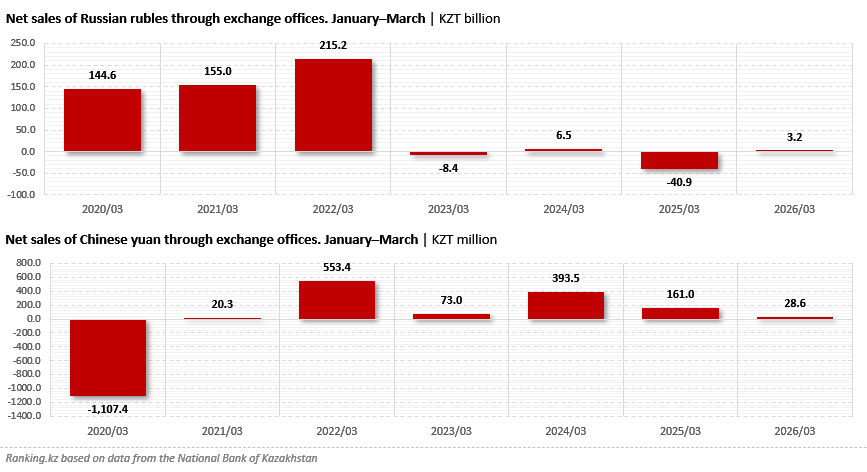

Net sales of Russian rubles to people in Kazakhstan have undergone a sharp reversal in trend over the past several years. While demand for the Russian currency remained extremely high in 2020–2022, before the escalation of geopolitical tensions surrounding Russia, the situation began to change rapidly after 2022. By the end of January–March 2022, net sales of Russian rubles through exchange offices had reached KZT 215.2 billion. However, already in the first quarter of 2023, the indicator turned negative for the first time, amounting to minus KZT 8.4 billion, meaning that sales of the currency by the population exceeded purchases.

Volatility persisted thereafter. In January–March 2024, the indicator briefly returned to positive territory, reaching KZT 6.5 billion. However, in 2025 the situation deteriorated sharply again, with the indicator falling to minus KZT 40.9 billion. The outflow was particularly noticeable in the second half of last year, when monthly figures dropped as low as minus KZT 53.2 billion. Against this backdrop, the beginning of 2026 appears more stable: by the end of January–March, net sales of rubles turned positive once again, reaching KZT 3.2 billion.

The situation with the Chinese yuan appears significantly calmer and more stable. Unlike the ruble, transaction volumes involving the yuan remain relatively small, while the overall dynamics are less volatile. While in January–March 2020 the indicator was negative, at minus KZT 1.1 billion, net sales returned to positive territory already in 2021. The peak came in 2022, when net sales of yuan reached KZT 553.4 million. In subsequent years, the figures declined, although they generally remained positive: net sales amounted to KZT 393.5 million in January–March 2024, KZT 161 million in the same period of 2025, and KZT 28.6 million in the first quarter of 2026.

Monthly dynamics for the yuan remain significantly less volatile compared to the ruble. Positive values were recorded in most months, while negative figures were localised and relatively small. At the same time, declines usually occurred in March–April — the period following the Chinese New Year, when business activity and trade volumes with China traditionally slow down. This may indicate that demand for the yuan in Kazakhstan is increasingly linked not to speculative fluctuations, but to real trade and settlement operations.